The City of Santa Clara appears to have figured out how to build a $1.02 billion public facility and get someone else to undertake virtually all the risk. Last week the City Council finally shared the details of the 49ers stadium agreement they have been hammering out for the last two and a half years.

“What makes this [project] unique… for the most part we’re not relying on any public assistance,” said Santa Clara Redevelopment attorney Tom Webber. “Facility revenues pay for the operating costs of the stadium and the debt costs.”

The financing deal with the 49ers unveiled at last week’s City Council study sessions – and likely to be approved by the time this goes to press – is that:

- StadCo, the 49ers stadium arm, will guarantee $850 million in construction loans from Goldman Sachs, U.S. Bank, and Merrill Lynch/Bank of America to the Santa Clara Stadium Authority (SA). StadCo is responsible for covering any cost overruns.

- No city, agency or SA funds, assets – including the stadium land – operating revenues, or enterprise funds will be used as be used as security for the loan. The collateral is, in essence, the 49ers – a business valued by Forbes in 2010 at $925 million.

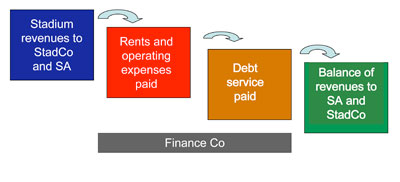

- Loans are repaid by stadium revenues, which include the annual facility rent paid by the 49ers. Currently estimated at $30 million, the actual rent will be set to cover stadium operating and debt expense.

- If the facility rent fails to cover expenses, the SA can convert the lease to make StadCo responsible for paying all the operating expenses (called a “triple net” lease).

- The 49ers must play home games at the stadium for the term of the lease (40 years) – called a “non-relocation” clause. If StadCo defaults on its obligations, the 49ers can’t play home games.

These terms are laid out in the 421-page draft Proposed Stadium Disposition and Development Agreement (DDA). (DDAs are contracts used to specify the terms of development projects on publicly owned property by private developers.)

The $850 million construction loan – from Goldman Sachs Bank; Merrill Lynch, Pierce, Fenner & Smith, Bank of America, N.A. and U.S. Bank National Association – will be made to a new entity, Stadium Financing Trust. The loan is expected to close in April 2012.

In turn, the Stadium Financing Trust, will lend $450 million to the Stadium Authority and $400 million to StadCo, which will advance this money as needed to the SA for construction. The loan will be disbursed as progress payments for completed work. StadCo will also purchase a portion of the Stadium Authority loan from the financing company when it matures (15 to 25 years).

The money is already available, Goldman Sachs managing director and head of sports facility finance Greg Carey explained at the study session. Carey’s experience includes financing the new Yankees and Giants-Jets stadiums.

“The NFL is different from any other sports league – it’s a great thing to have the NFL as a creditor,” he said. “When we’re lending money how we’re getting paid back is [by] the stadium opening and revenue flowing in.

“This loan is structured so that there’s only a one percent charge for money that’s committed and not drawn,” Carey continued, adding that he expected only $650 million of $850 million to be actually drawn on for the construction.

The Stadium Authority, in turn, will pay back the loan from its revenues, including: naming rights, seat licenses – the right to buy season tickets for a certain seat in the stadium, called Stadium Builders Licenses (SBLs) – half of net non-NFL event revenue, and ticket surcharges (yet-to-be-established for NFL events, and $4 per ticket for non-NFL events). Stadium revenues during construction will be used to prepay the loan and when the debt is repaid, the SA will retain the revenue for ongoing expenses.

“Rent payment would service that loan,” 49ers Chief Financial Officer Larry MacNiel said at the Dec. 6 study session. “It’s all inside the StadCo-SA relationship, which is ultimately supported by rent. The rent will not be set until the stadium is operational. If our projections are wrong, the SA can put those operating costs back on StadCo.”

The deal is structured to pay the stadium city rents and operating and maintenance expenses (O&M) first. Debt service then is paid and any additional revenues return to the SA and StadCo.

Much of the deal’s complexity results from the requirements of Measure J – the 2010 Santa Clara ballot initiative approving the stadium project. It specified that stadium financing must be structured in such a way as to absolutely shield Santa Clara’s general and enterprise funds from any liability, and protect public land ownership.

And if things go sour?

“The city’s rights under the ground lease are protected,” said Webber. “Whoever would step into stadium authority is still obligated to pay rent – if they don’t pay they would be evicted. An exigency we really haven’t talked about [is that] the NFL will step in and help sort things out. Any new entity that comes in will have to live up to the [agreement’s] conditions.”

The guarantee for this is the contract’s non-relocation clause, Webber explained. If the 49ers don’t pay the rent, they can’t play home games in the stadium; but because of the non-relocation agreement, they can’t play home games anywhere else.

“The underlying asset behind this is the 49ers team itself,” said Stanford Business School professor George Foster, co-author of “The Business of Sports.” Foster teaches sports business management and has conducted NFL-Stanford executive education workshops. “The underlying strength of the NFL should not be underestimated. They can always sell a partial equity in that. In my opinion, the numbers being presented here are conservative.”

Information about the proposed 49ers stadium project is available at santaclaraca.gov/index.aspx?page=1197. City Council agenda reports can be found at santaclaraca.gov/index.aspx?page=1359. You can watch video of the Dec. 6 and Dec. 8 study sessions at santaclaraca.gov/index.aspx?page=43.

Santa Clara Football Stadium Financing in a Nutshell

- Up to $850 million loan to StadCo and Santa Clara Stadium Authority: to be repaid from stadium revenues.

- Up to $40 million from the Santa Clara Redevelopment Agency: to be repaid from RDA property tax increment. (An RDA tax increment is the amount that property tax revenues increase after a redevelopment project; these are used to repay development bonds).

- About $150 million tenant improvements paid for directly by StadCo.

The total of these sources, $1.04 billion is actually slightly higher than the estimated construction cost of the stadium, $1.02 billion.

0 comments